Mortgage Refinancing · NZ-Wide

Refinance Your Mortgage

with Confidence

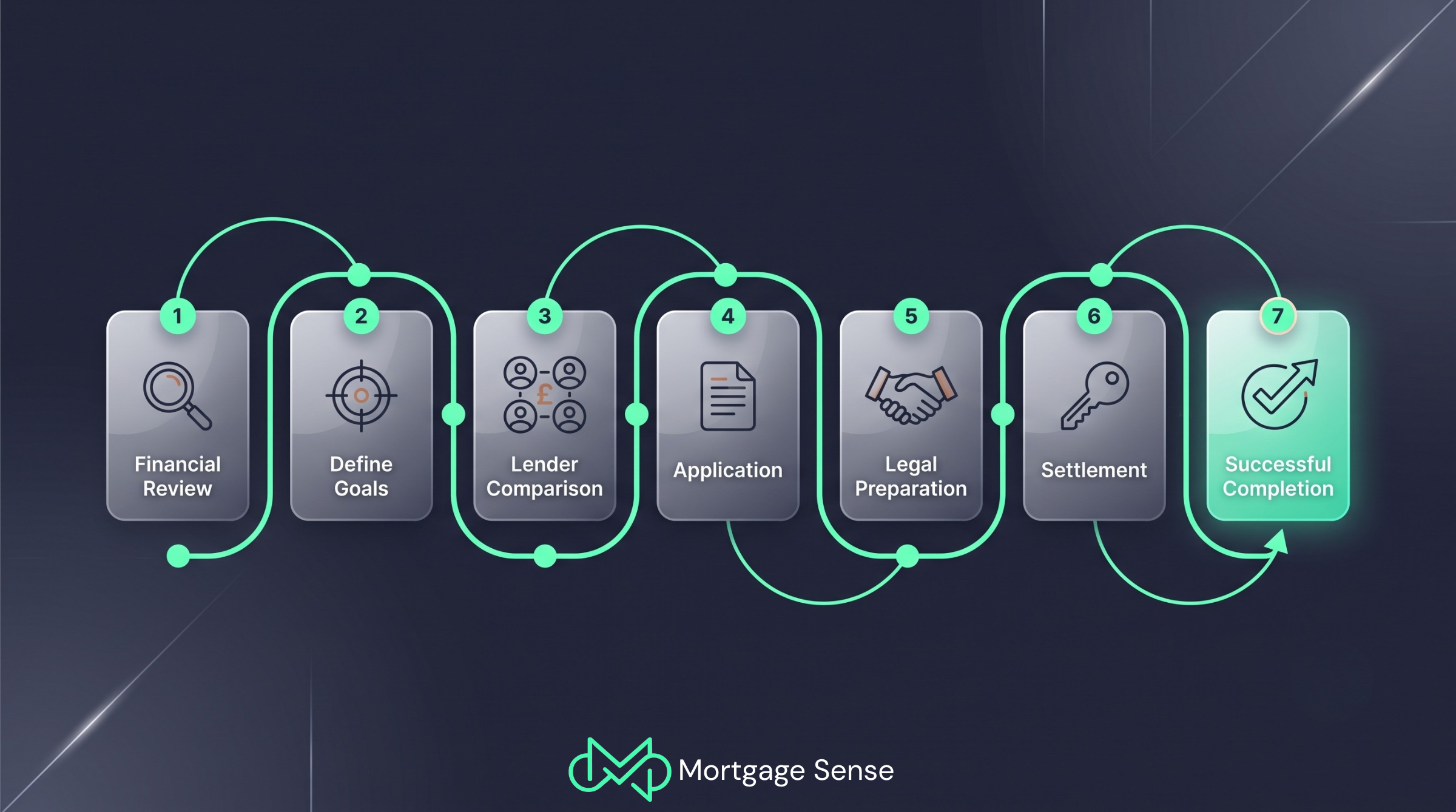

Looking to refinance your mortgage? We help NZ homeowners refinance their mortgage to save on interest, access equity, or consolidate debt — finding the right strategy for your situation.

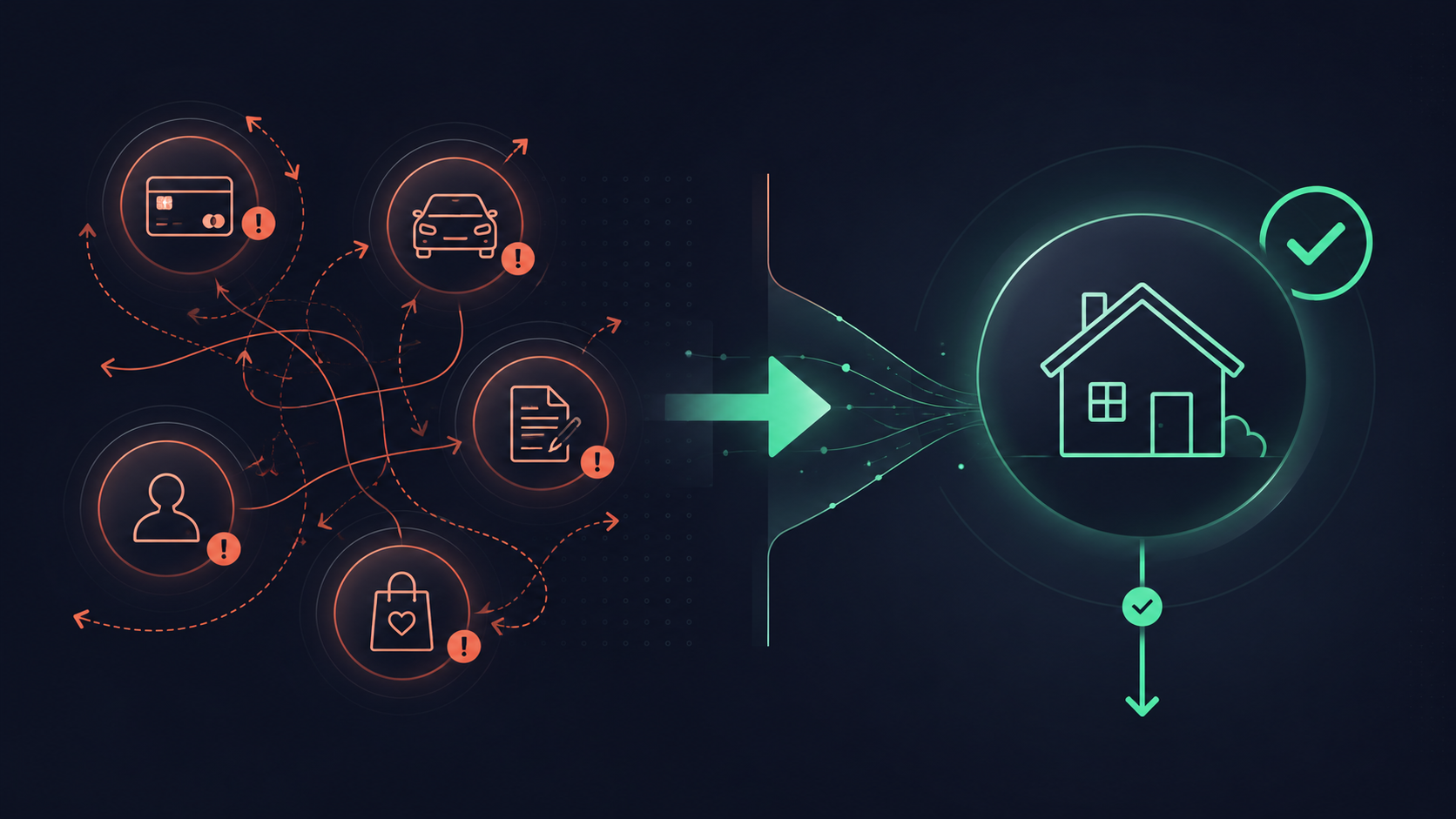

Refinance your mortgage in New Zealand to reduce interest payments, access equity, or consolidate high-interest debt. We work with 30+ lenders to find the right refinancing solution for your situation.