Bad credit home buyers

Bad credit doesn’t mean no.

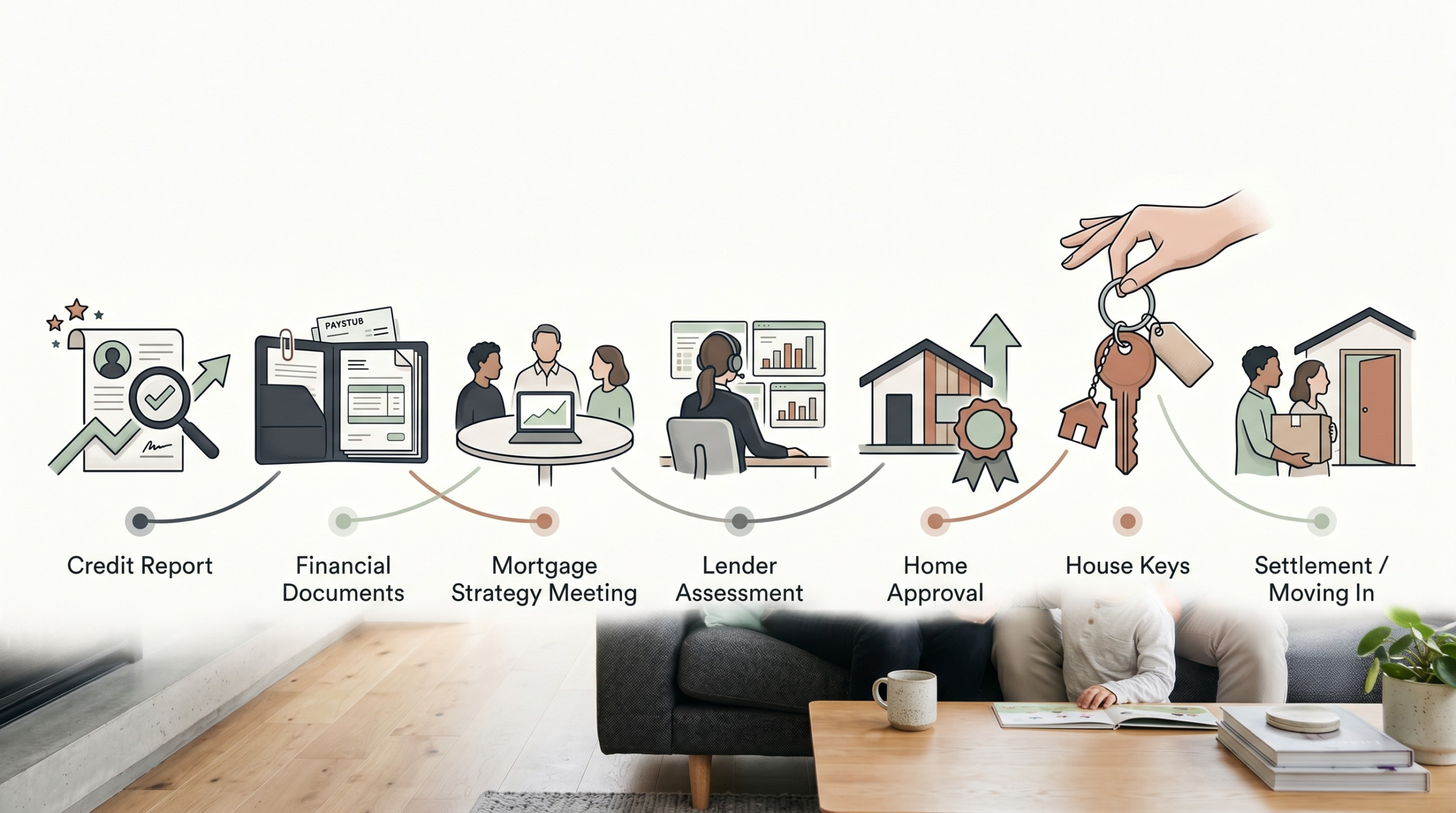

Your credit history is one part of your story — not the whole story. A bad credit mortgage is often still achievable, and we help borrowers with imperfect credit find lenders who look at the full picture.